Stocks Lead Change

US stocks broadly extended their losses through March, following a decline in February, as investors remained cautious ahead of significant US trade tariff actions. The introduction of increased trade barriers may hamper global output, restrict economic growth, and raise consumer prices—all critical factors that can negatively impact stock market valuations.

Before trade tariff news took center stage, investors paid about 20 times the broader earnings of US large-cap stocks, a standard metric used to gauge stock market valuations. This price-to-earnings ratio can also be viewed as a yield, with 1 divided by 20 indicating an expected return of roughly 5% from US large-cap stocks over the next 12 months. However, the US tariff proposals challenge these earnings estimates, as tariffs could temporarily depress earnings, reducing returns below the anticipated 5%. In addition, investors may recalibrate their expectations, adjusting stock market multiples downward in response to the rising uncertainty. Instead of a 20-times multiple, a more plausible equilibrium might emerge around 17, reflecting the growing risks.

“It’s crucial to remember that positive market movements can often follow periods of negative volatility. To recover and capitalize on growth, investors must remain patient, resist the urge to sell impulsively, and avoid behavioral mistakes during volatile times.”

These declines in the stock market are likely driven by a combination of anticipated earnings contraction due to tariffs and investors’ reluctance to offer high multiples in the face of uncertain economic conditions. Historically, stock market declines often precede earnings losses, while stock market gains tend to occur before economic recoveries and the return of earnings growth. Major disruptions, like US tariffs, necessitate significant adjustments by investors and businesses, requiring time for markets to restructure. As a result, investors may experience short-term losses as they adapt to these changes.

It’s crucial to remember that positive market movements can often follow periods of negative volatility. To recover and capitalize on growth, investors must remain patient, resist the urge to sell impulsively and avoid behavioral mistakes during volatile times. While it may be tempting to react to short-term declines, maintaining a long-term perspective is key to navigating market challenges and emerging stronger.

Tariffs

President Trump has been referring to April 2 as “Liberation Day,” which is the date that he enacted “reciprocal tariffs” on a large number of countries. As of April 5, 2025, foreign imports sold in the US will be forced to pay a minimum baseline tariff of 10%. The rate is higher for specific countries, depending on the trade imbalance between the US and each foreign partner, which is based on a variable rate formula.

The incremental tariff rate increases on foreign goods and services shipped to the US for consumption are significant. Previously, US tariffs broadly averaged about 2.5% on all imports, but these new tariffs would result in US tariff rates rising as high as 22.5%.

The immediate tariff effects are expected to increase consumer prices, decrease global growth, and be partially responsible for recent losses in business optimism. Professional estimates vary, but they suggest that the recent tariff increases could detract from corporate profits, similar to the potential impact of a corporate tax increase.

The US tariffs may be short-lived if other countries negotiate, which is the hope. There have been varying responses, but a large number of countries immediately began seeking negotiations with the US. The most notable retaliatory response is from China. The US and China have now gone back and forth multiple times with retaliatory tariffs. Currently, both countries have increased tariff rates to such levels that it would likely stall much of any trading activity.

On April 9, Trump surprised markets yet again with a 90-day pause on the full implementation of the new tariffs. The 10% baseline tariff will still be effective, but the additional tariffs are being suspended, except for those tariffs involving China, due to the country’s retaliatory response. This could be the beginning of a major decoupling of the world’s two largest economies.

April 2 was the start of a new normal for asset price volatility in the markets. Stocks have been swinging wildly, mostly to the downside. However, April 9 posted one of the largest positive single-day stock market returns in history after Trump announced the 90-day tariff pause. Both the stock and bond markets are desperately trying to quantify the price impacts of the tariff-related uncertainty.

Inflation & Employment

Inflation data is being closely watched to see signs of tariff-related impacts. The Producer Price Index, or PPI, was unexpectedly unchanged for the month of February. PPI measures the costs of inputs for producers, which is often used as an indication of future inflation for consumers.

The Fed’s preferred inflation measure, the Personal Consumption Expenditures, or PCE index, rose slightly higher than expected in February. Over the trailing year, PCE rose 2.8% as of February, up slightly from January.

March Consumer Price Index, or CPI, data was recently released, which surprised markets with a lower-than-expected reading. The trailing one-year CPI data showed prices increased at a rate of 2.4%, one of the lowest readings in quite some time. This was surely good news for the markets, but was masked by all of the tariff-related news.

The US labor markets continue to show signs of strength. The March jobs data came in stronger than expected and stronger than the month prior. However, unemployment ticked slightly higher from the prior month. Again, this is good news for the markets, but it was overshadowed by all of the activity related to global trade.

Monetary Policy

The Fed decided to hold interest rates at current levels in its most recent policy meeting, maintaining benchmark rates in the 4.25 to 4.5% range. This is the second meeting in a row in which rates remained unchanged.

It may now be a bit optimistic to expect two rate cuts this year, as many Fed officials expect one cut or no cuts for the year. The Fed has become less optimistic about inflation and economic growth. Specifically, its expectations for inflation have risen, and for economic growth have declined. However, the Fed acknowledged that economic growth has been solid.

Fed Chair Powell was quite articulate that Trump’s trade agenda would likely increase inflation, but the magnitude and duration are yet to be seen. Powell stated that inflation had approached the Fed’s target but that progress may now be delayed. Tariff-related inflation may prove to be “transitory” or temporary. Treasury Secretary Bessent is a big advocate of that belief. Powell originally indicated that his current base case for the tariff-induced inflation was also that it would be transitory. However, he has more recently retreated from that stance and is indicating that this inflation could be more persistent based on the larger-than-expected tariffs.

Powell continues to articulate a “wait and see” monetary policy approach, indicating the Fed needs to better understand the impact of tariffs and other policy developments from the new administration before cutting rates further. Although the recent Personal Consumption Expenditures (PCE) Index data wasn’t significantly higher than expected, it was slightly higher than expected. This further indicates that the Fed may need to wait even longer than expected, especially when considering the uncertainty associated with tariffs.

“As a reminder, the Fed’s ‘dual mandate’ is price stability and maximum employment, which will surely become a trickier balance in light of the global economic rebalancing that is now in full swing.”

Powell continues to articulate a “wait and see” monetary policy approach, indicating the Fed needs to better understand the impact of tariffs and other policy developments from the new administration before cutting rates further. Although the recent Personal Consumption Expenditures (PCE) Index data wasn’t significantly higher than expected, it was slightly higher than expected. This further indicates that the Fed may need to wait even longer than expected, especially when considering the uncertainty associated with tariffs.

As a reminder, the Fed’s “dual mandate” is price stability and maximum employment, which will surely become a trickier balance in light of the global economic rebalancing that is now in full swing.

Finally, a new development recently unfolded, and President Trump started pressuring the Fed on its monetary policy decisions. Specifically, Trump stated on multiple occasions that the Fed would be better off reducing rates as tariffs begin taking effect. Trump went on to tell Powell specifically to cut rates and to “stop playing politics.” In Powell’s recent press conference, he explained that he always wears purple ties because it’s a good color to communicate that he is nonpolitical!

Stocks

Stocks have been hit hard by the uncertainty resulting from the new tariffs. As the tariff environment has quickly evolved, stock markets have been trying to price in the related impacts. Stocks have now experienced regular swings of 5 to 10% on a daily basis since April 2. As more clarity and definition fall onto the future of global trade, markets will very likely settle down. But in the meantime, we expect continued volatility.

It is important to note that volatility is not synonymous with market loss. April 9 was a great example of upside volatility, where news broke about tariff delays, and markets responded with near 10% returns. It is incredibly important to control behavioral biases and refrain from making erratic investment decisions during times of market stress. Even missing returns from single market sessions can negatively impact long-term returns if those decisions are improperly timed.

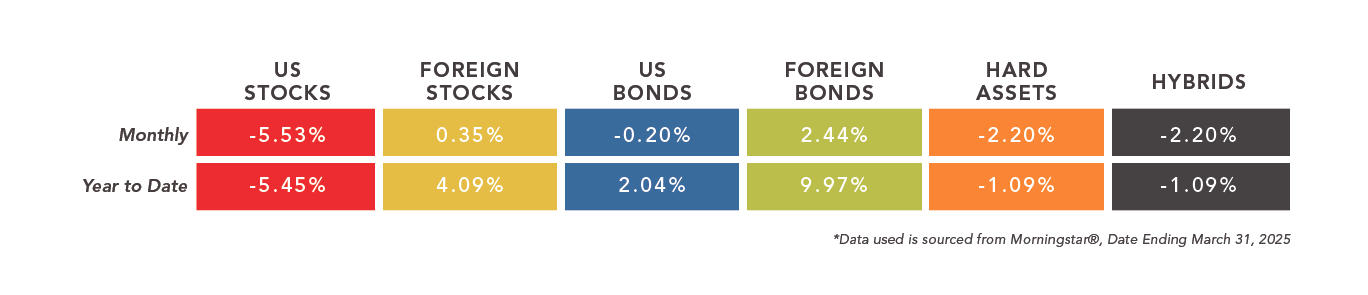

Global diversification has again been supported over the recent past. Foreign stocks have been surprisingly stable during the recent volatility in the stock market and have been outperforming US stocks by a sizeable margin since the beginning of the year.

Bonds

Although stock market volatility has been a highly publicized event related to tariff pressures, bond yields have also been significantly impacted. When demand for bonds is lower, their yields generally increase, and prices usually fall. Specifically, 10-year treasury yields have increased quite dramatically since April 2, which may be an indication of investors reconsidering these assets as a “safe haven.” The trade tensions between the US and China seem to be the major driving force behind these yield increases and price declines. Throughout this type of global turmoil, the fact that treasury yields are rising could indicate that something is fundamentally shifting.

Yield volatility is impacting long-term bonds more than short-term bonds. This is leading to larger price declines in long-term bonds relative to bonds with shorter-term maturities. This has been yet another hit to longer-term bonds after the lengthy rate hike cycle from the Fed.

Higher-yielding bonds have been negatively impacted by the same factors driving equity market volatility, but have been more resilient than longer-term bonds. Yet, there are some growing concerns that the new tariffs will impact high-yield bond issuers’ ability to repay debt in the future. This is another implication of tariffs that needs to be closely monitored.

Foreign bonds have generally been more resilient than US bonds during the tariff-related developments. This is a departure from recent trends, as US bonds have been outperforming the global markets for quite some time.

© Advisory Alpha. Registration with the SEC or state does not constitute an endorsement of the firm by regulators, nor does it indicate that the adviser has attained a particular level of skill or ability. This content is for informational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any securities. Investing involves risk, including the potential loss of principal. No investment strategy, such as asset allocation or diversification, can guarantee a profit or protect against loss in periods of declining values. All investment strategies involve risk and have the potential for profit or loss. Changes in investment strategies, contributions or withdrawals, and economic conditions may materially affect the performance of your portfolio. There are no assurances that a portfolio will match or outperform any particular benchmark. Investors should carefully consider the investment objectives, risks, fees, and expenses before investing. Any financial services firms referenced in this material do not provide tax or legal advice. Please consult with your tax or legal professional regarding specific issues prior to making a tax or legal decision.

The performance information presented in the asset category section of this report is based on equal-weighted averages of the following Morningstar Categories: US Stocks (US Fund Large Blend, US Fund Mid-Cap Blend, US Fund Small-Blend), Foreign Stocks (US Fund Foreign Large Blend, US Fund Foreign Small/Mid Blend, US Fund Diversified Emerging Mkts), US Bonds (US Fund Intermediate Government, US Fund Inflation-Protected Bond, US Fund Corporate Bond, US Fund High Yield Bond, US Fund Bank Loan), Foreign Bonds (US Fund World Bond, US Fund Emerging Markets Bond), Hard Assets (US Fund Commodities Precious Metals, US Fund Commodities Energy, US Fund Global Real Estate, US Fund Real Estate), Hybrid Assets (US Fund Convertibles, US Fund Preferred Stock).

© 2025 Morningstar. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete, or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results. Morningstar category data is provided for illustrative purposes only to demonstrate a hypothetical investment vehicle represented by a group of similar investments. Morningstar category data is an aggregation across actual funds contained in the category, but it is not possible to directly invest in a category. Index returns are provided for illustrative purposes only to demonstrate a hypothetical investment vehicle using broad-based indices of securities. Unmanaged indexes are not available for direct investment. All data shown does not include internal fund expenses, trading costs, financial advisor fees or commissions, or taxes. This information is not intended to predict the performance of any specific investment or security. Past performance is no guarantee of future results.

Bureau of Labor Statistics. Unemployment Rate, Total Nonfarm Employment, Labor Force Participation, Consumer Price Index, Producers Price Index. www.bls.gov. United States, Department of Commerce, Bureau of Economic Analysis. Personal Consumption Expenditures, Gross Domestic Product, Consumer Spending, Personal Income and Outlays. www.bea.gov. Federal Reserve. Fed Funds Rate, Fed Funds Target Range, Minutes of the Federal Open Market Committee, Board of the Federal Reserve System Calendar. www.federalreserve.gov. Trump, Donald. @realDonaldTrump. Truth Social.

Cole, A. “Trump’s Reciprocal Tariff Calculations Are Nonsense, Will Punish Mutually Beneficial Trade”, Tax Foundation, 3 April 2025, taxfoundation.org/blog/trump-reciprocal-tariffs-calculations/. Drumm et al. “The New US Tariffs”, G|M|F, 7 April 2025, https://www.gmfus.org/news/new-us-tariffs. Cembalest, M. 2025 Eye on the Market Outlook, Redacted: Straight talk from the CEO front lines on Liberation Day,” J.P. Morgan, 2 April 2025, page 5.